'Sooner or later we all sit down to a banquet of consequences'

Robert Louis Stevenson

Successive UK governments have for almost four decades been recklessly indifferent to the UK’s persistently low savings and investment, justified by the myth that it is not a priority for a services-led economy and that we can instead rely on continuous access to capital from overseas.

While other factors have been at play, this has left the UK with:

- 15 years of stagnant per capita income (0% growth), a fall of 12 places (to 23rd) in the UK’s global ranking

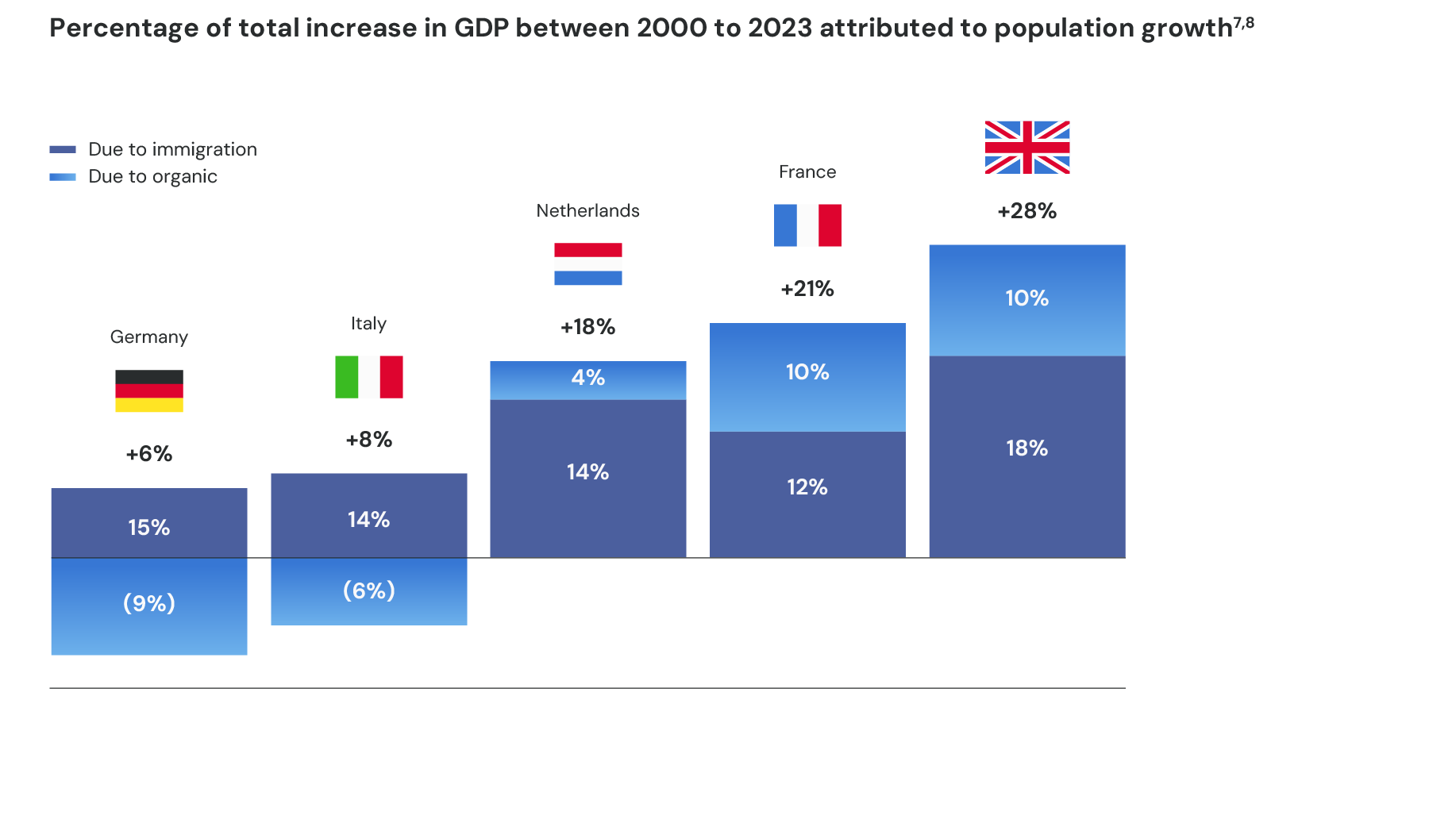

- an economic growth recipe and fiscal position which is unsustainably reliant on immigration (10+ million gross since 2000)

- an irresponsible dependence on foreign capital, leading to debacles such as Thames Water

A total reorientation of public policy to the rebuilding of the UK’s savings and investment is urgently required.

This will enable us to restore per capita income growth, recover economic competitiveness and national sovereignty, and assure adequate retirement provision for today’s and future generations.

The time to act is now.

It is a myth that a services-led economy does not require savings and investment – UK savings levels are significantly lower than peers, who are similarly dependent on services

The persistence of this myth paved the way for a succession of bad policies that destroyed the DB pension system, allowing the insurance industry to feast on its remains

‘It’s worse than a crime, it’s a blunder’

Comment in reaction to Napoleon’s execution of the Duc d’Enghien in 1804 by Joseph Fouché or Antoine Boulay de la Meurthe (also often credited to Voltaire)

Governments then took over a decade to implement a replacement, DC auto-enrol, which is totally inadequate to meet future retirement needs and even more fragmented and underweight UK assets than the existing DB system

One of the many consequences of the DB system’s destruction has been the collapse of UK equity valuations, with UK companies now at a massive competitive disadvantage, especially raising new capital for growth

UK per capita income has been stagnant for over 15 years. The only period of robust growth was during the Bubble, fuelled by unsustainable leverage

'It is a night of disaster when a man sees the truth'

Bertolt Brecht

As a result, the UK’s global per capita income ranking has fallen 12 places, more than any other major country, with the UK now in 23rd place

‘We’re unable to see the face of the mountain while we stand on top of it’

Old Chinese proverb

This dismal per capita growth record cannot be attributed to the UK’s overall taxation levels, which have been consistently lower than our peers (and an unchanged 45% top rate since 2013)

UK Governments’ revealed preference: Tax hikes? Spending cuts? Or higher legal immigration? Without the last decade’s immigration, UK income tax revenues would today be ~£14bn lower

‘David Miles, executive member of the Office for Budget Responsibility (OBR), has warned that a migrant-driven upgrade to the UK’s population may not provide a long-term boost to the public finances’

The UK economic growth is more dependent on immigration than any of our major European peers

Dependence on foreign capital has also led to a steady erosion of the UK’s national and economic security, best illustrated by Thames Water

Reservoir of domestic capital is vital to safeguarding critical national assets

Critical infrastructure

- Much of UK’s water, rail and transport industry is owned by foreign capital (e.g. Thames Water, Heathrow Airport)

- Almost all major UK projects entirely reliant on foreign capital (e.g. HS1, wind farms, solar power, toll roads)

Energy security

- Five out of the six main UK energy companies, and all of our gas distribution under foreign ownership

- Nuclear (Sizewell C) half owned by non UK interests with remaining stake previously under Chinese ownership

Technology industries

- DeepMind sale to Google, ARM Holdings sale to SoftBank and subsequent US listing

- Newport Wafer Fab (NWF) owned by Wingtech Technologies (HK)

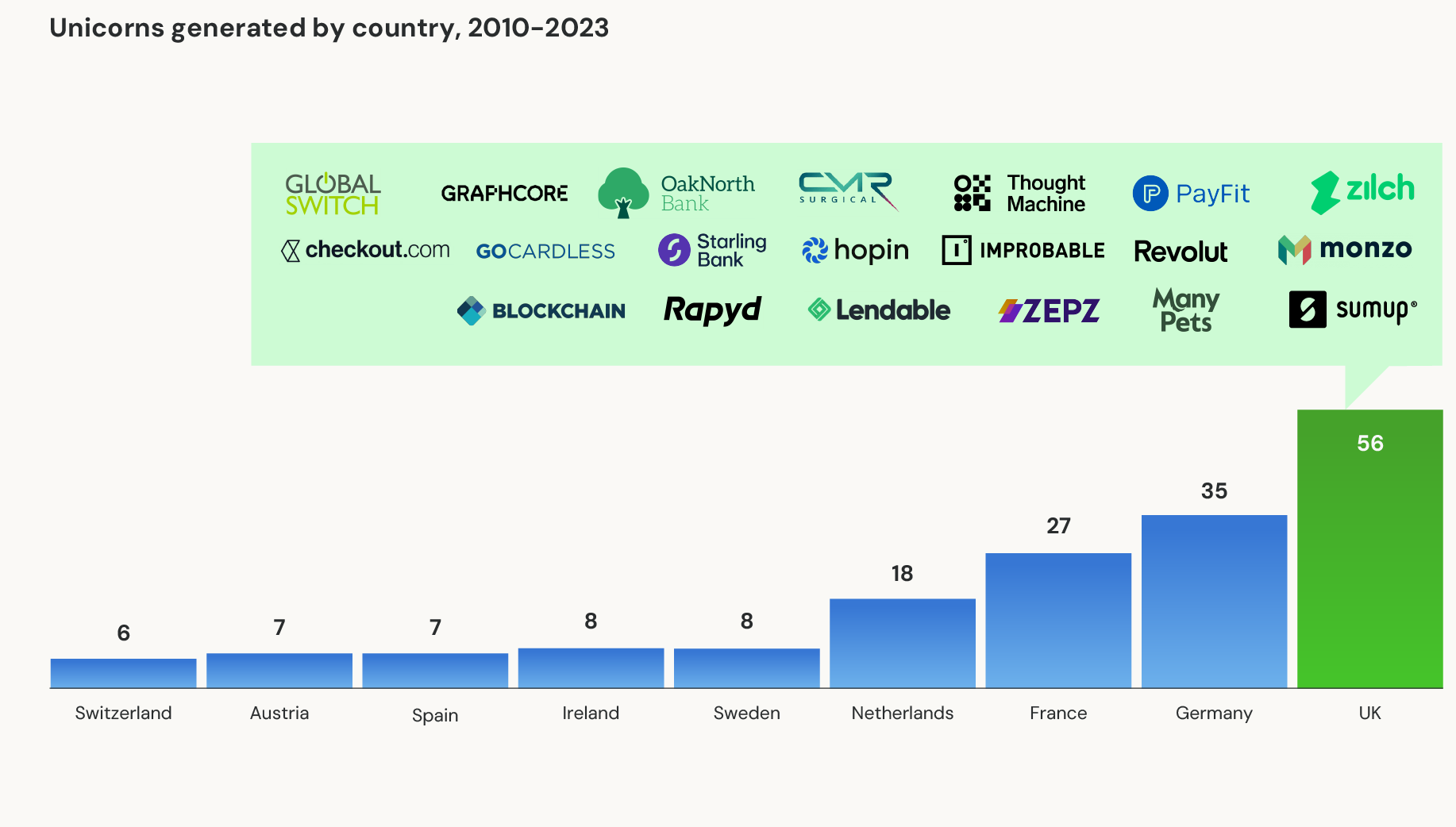

'Tomorrow's winners'

- Every significant new UK enterprise financed by foreign venture capital, including Graphcore, CMR Surgical and Hopin

- Most of wealth being created by new companies will accrue outside the UK

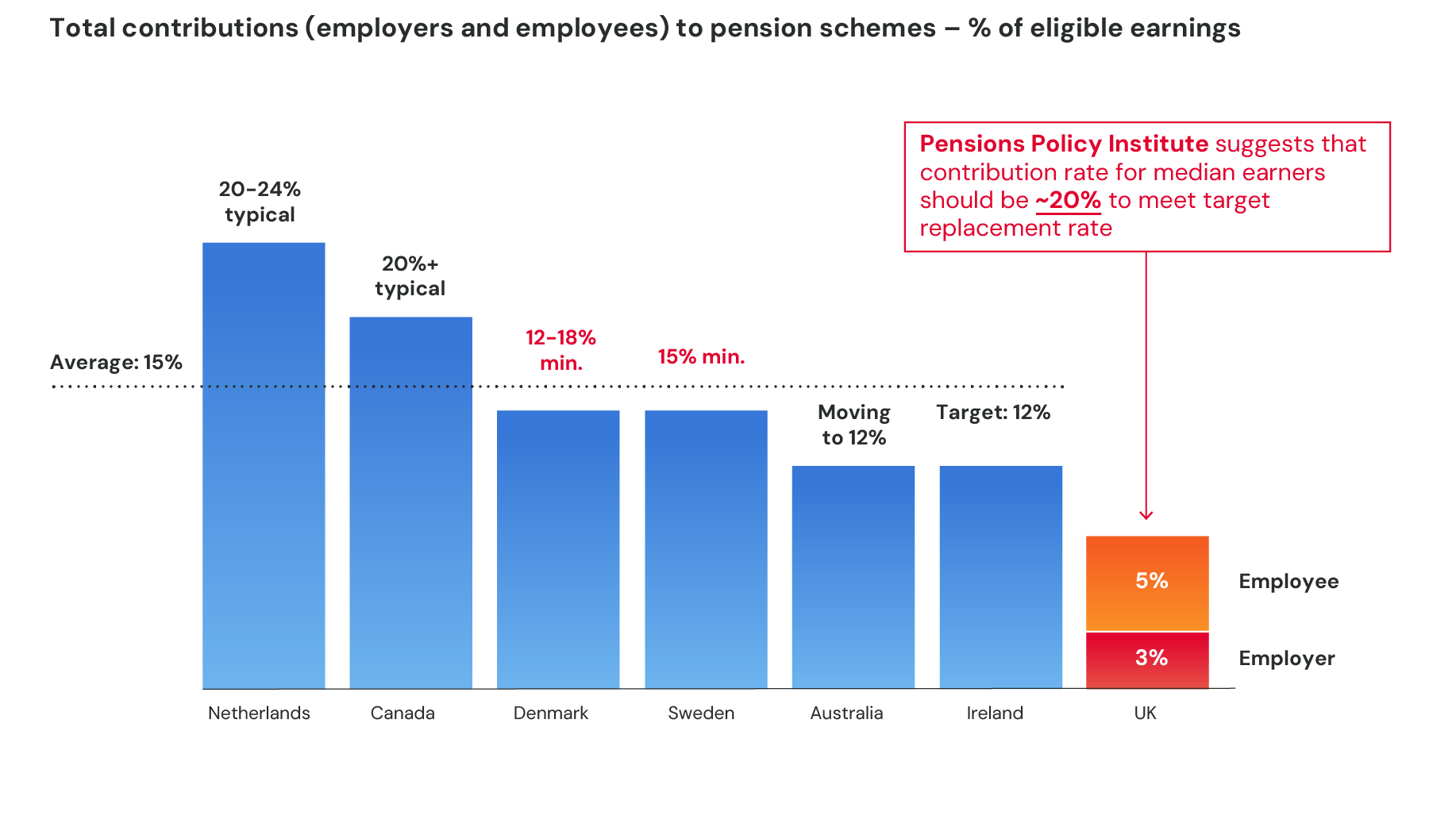

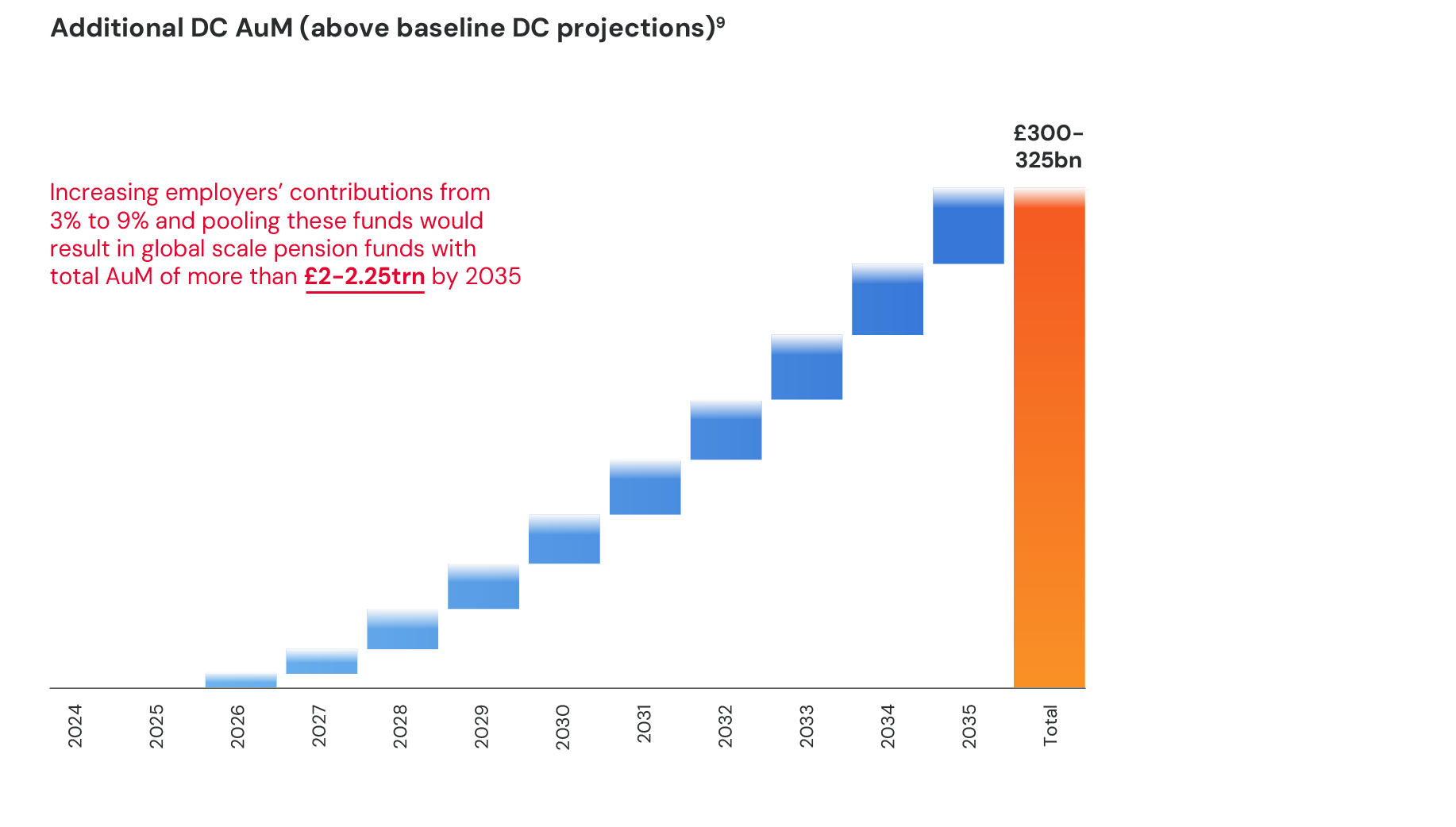

A step change increase in employers’ contribution to DC auto-enrol, while pooling the fragmented schemes (and streaming a portion to invest in UK assets) to enable adequate retirement provision for future generations – a critical first step

Higher DC auto-enrol consolidated and streamed as for 20% into UK corporate assets plus tying UK asset allocation to DB pension funds’ tax privileged status would generate £300bn+ of new productive investment for the UK

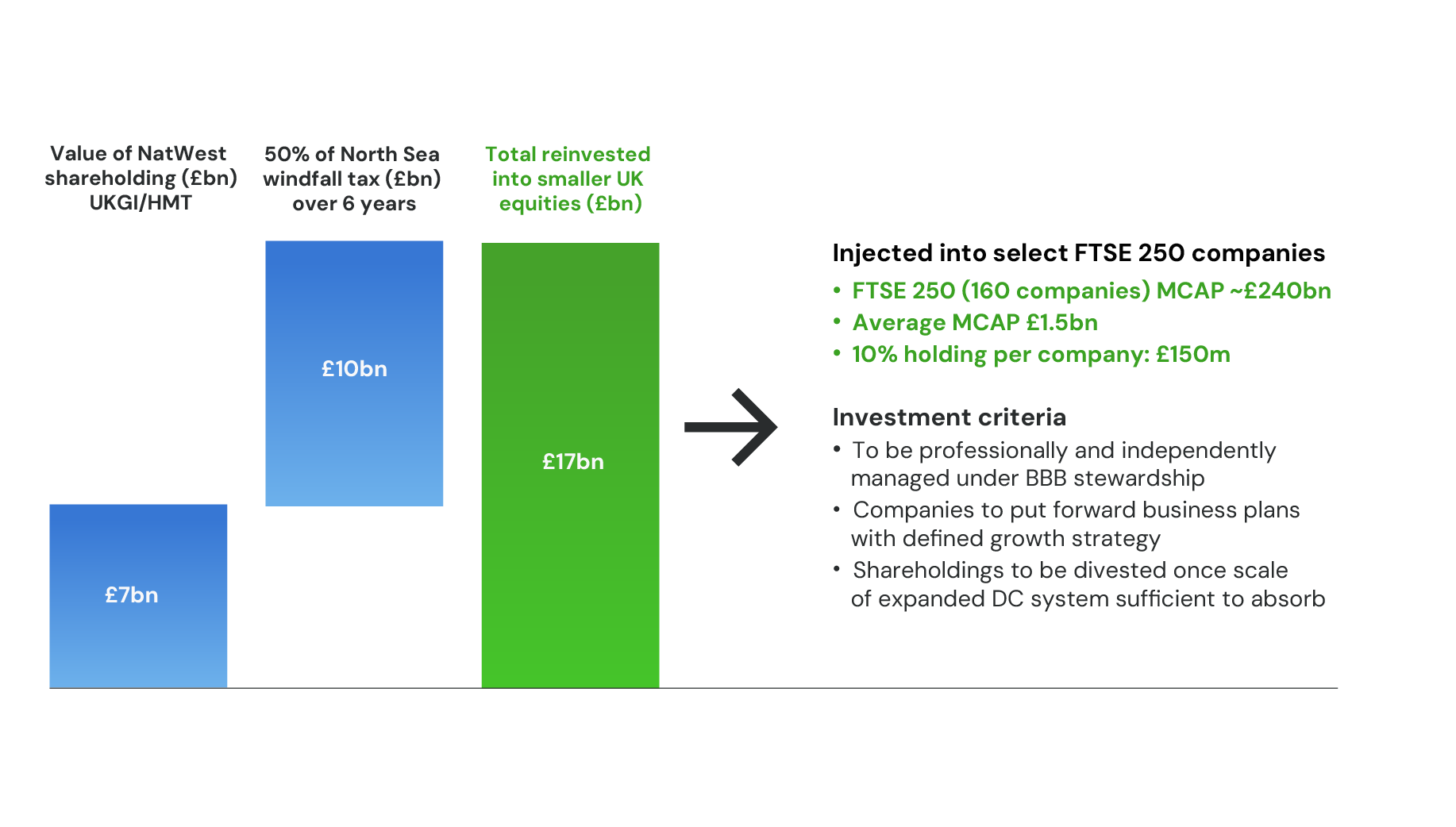

As it will take time to re-build the domestic equity reservoir, a redeployment of NatWest sale proceeds and North Sea windfall tax can serve as a nucleus for a new sovereign wealth fund, providing much needed capital to UK smaller listed companies in the market

The remaining DB pension system cannot be permitted to be liquidated through insurance buyouts, both to preserve UK productive investment and to protect the stability of the gilt market. A windfall tax on excess returns from buyouts is necessary and justified

Greater incentives for capital investment/R&D would help stimulate investment for the long-term rebalancing of the UK economy, and restore industrial competitiveness

The UK is by far the and away the European leader in the number of private companies valued at >$1bn. However, the wealth and value creation accrues mostly overseas

Enhanced incentives for individuals to start and grow businesses will stimulate growth and keep more of the wealth creation from the UK’s energy and creativity here at home

1

More businesses are started per capita in the UK than in any other European country, in addition to having by far the most ‘Unicorns’ (private businesses valued at least $1 billion)

2

£1m per person lifetime deduction for income tax purposes (or, if insufficient taxable income, a transferable credit as per the US Inflation Reduction Act) for all investments in UK startups or private trading companies with a minimum holding period 3 years (up to 50% may be deductible in any one year)

3

The sale of any such investment would also be exempt from tax on capital gains (currently 10%) and from Inheritance Tax of up to £1m per person per lifetime

4

Any business (other than real estate or regulated financial services) would qualify, in line with the overall goal of encouraging both new business creation/replenishment and rebalancing as between industry and financial services

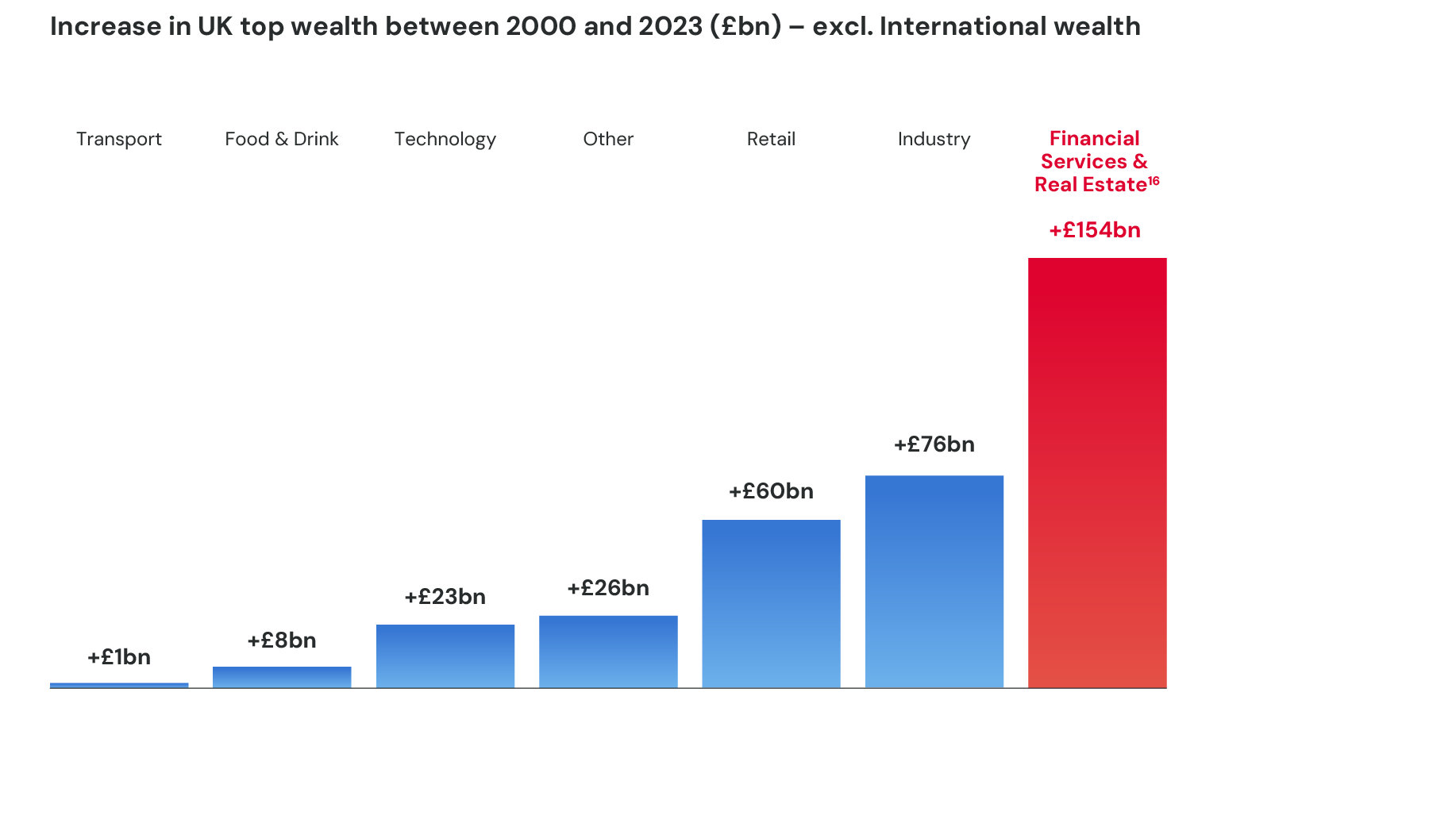

This will also help restore a better and more diversified balance of wealth creation, which has favoured financial services and real estate

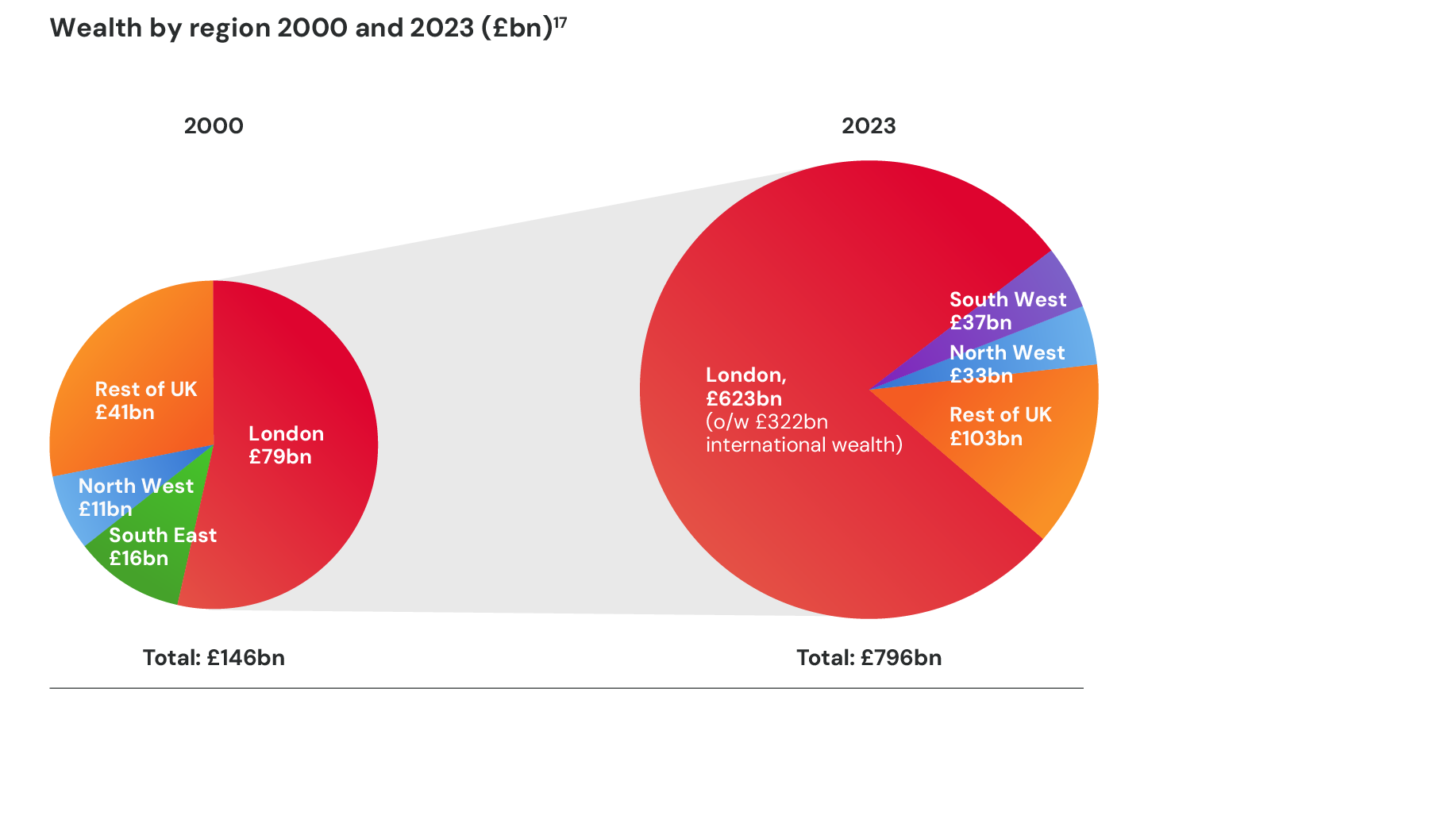

More domestic savings to harness the UK’s abundance of entrepreneurial energy and capacity for innovation will lead to wealth creation which is better aligned with the distribution of talent around the country

A total reorientation of public policy towards an urgent rebuilding of the savings and investment system that is critical to restoring per capita income growth and our sovereignty

Savings for life

A material increase in the employer’s contribution to DC savings plans to begin both the rebuilding of the savings pool and to provide better retirement security for the next generation, accompanied by an aggregation into a global scale pool

Kickstart

Kickstart a sovereign wealth fund through an immediate injection of new capital into the domestic equity market (from 50% of the North Sea windfall and NatWest sale proceeds) with an initial focus on FTSE350

Refilling the reservoir

Replenishing the reservoir of domestic equity capital by linking DB and DC pension funds’ tax privileges to minimum investment in UK domestic assets (companies and infrastructure)

'Dead money' tax

A new ‘dead money’ tax to protect the remaining DB pension schemes from buyout related liquidation and its consequences for the UK’s domestic equity and gilt markets

Investment for growth

A rebalancing of the tax system between capital investment/R&D and labour to improve productivity and reduce the economy’s dependence on immigration

Entrepreneurs unbound

Unleashing and amplifying entrepreneurial activity through a lifetime allowance of £1m per person deductible from income for tax purposes, up to 50% in one year

Comments

Comment Guidelines

Please keep comments respectful. Use plain English and avoid using phrasing that could be misinterpreted as offensive. By commenting, you agree to abide by our terms and conditions. We encourage you to report inappropriate comments.